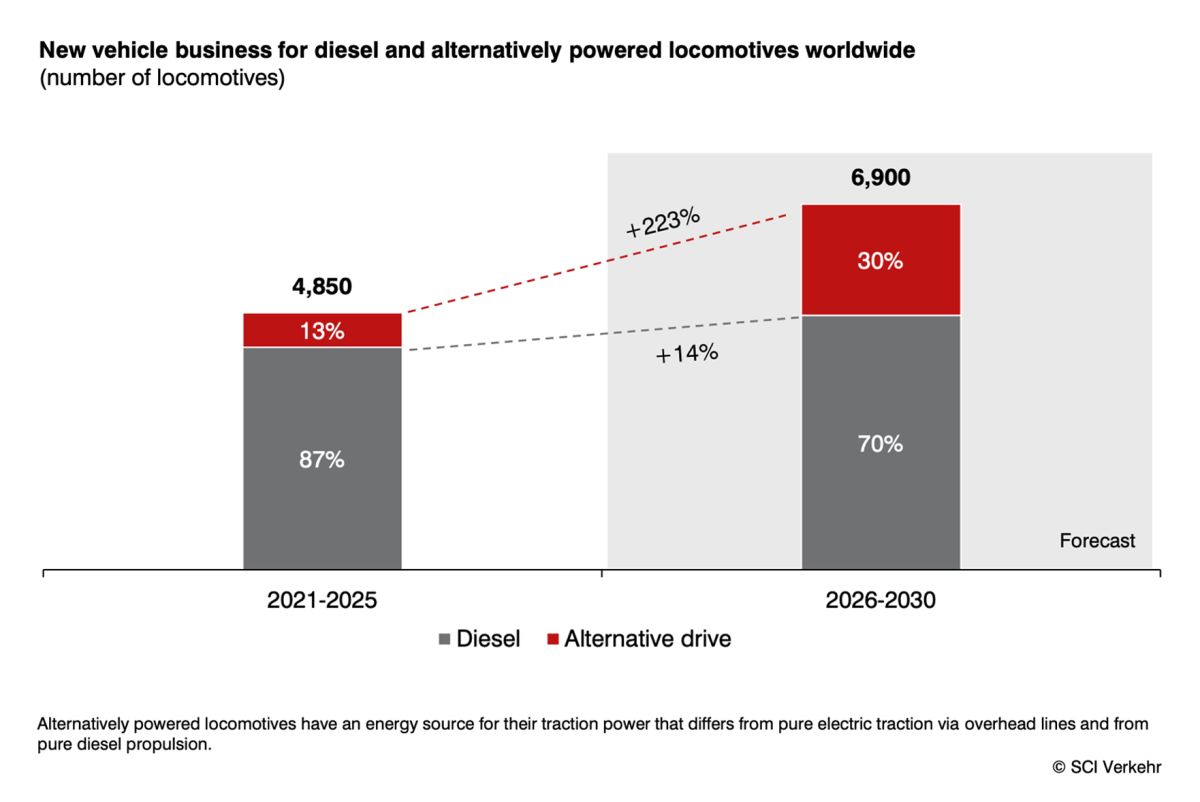

The transition towards greener locomotive fleets is progressing more slowly than expected, with diesel traction remaining operationally indispensable for rail freight operators. This is the main conclusion of the latest SCI Verkehr study on diesel and alternative-drive locomotives.

In Europe, diesel locomotives continue to play a central role, particularly in shunting operations and on non-electrified branch lines and marshalling yards. Although hybrid and dual-mode locomotives are technically available, rail freight operators face strong economic pressure, especially in single wagonload traffic, where margins remain limited.

The study highlights higher acquisition costs as a key obstacle for alternative-drive locomotives when compared with conventional diesel units. In addition, lengthy and complex approval procedures are delaying market entry, with several procurement projects reportedly cancelled despite earlier plans to deploy greener traction.

Globally, growth in locomotive demand is driven primarily by fleet replacement rather than a rapid technological shift. While the share of alternative-drive locomotives is expected to increase gradually, diesel units are still forecast to account for the majority of new freight locomotive purchases in the coming years.

Regional differences remain pronounced. Western Europe has seen increased activity linked to deliveries of dual-mode mainline locomotives, while Asia, particularly China and India, continues to focus on large-scale network electrification. In contrast, regions with low electrification levels — including parts of Africa and Australia — are expected to rely on diesel traction well into the next decade. With only around one third of the global rail network electrified, overhead-line-independent locomotives remain essential for freight transport worldwide.

FACT BOX — Freight Locomotive Market

- Global market value (2025): ~EUR 3.8 billion

- Forecast market value (2030): ~EUR 4.5 billion

- Main growth driver: Fleet replacement

- Electrification of global rail network: ~33%

- Key barriers for alternative drives: Higher purchase costs Complex approval procedures

- Higher purchase costs

- Complex approval procedures

- Diesel role: Remains dominant in freight, shunting and non-electrified network