Based on feedback from industry operators and insights gathered through a social media poll by Railmarket News, the challenges facing this mode of transport remain consistent across countries. Operators cite high operational costs, intense road competition, and fragmented infrastructure management as ongoing concerns. Some companies also pointed to modernization needs, inconsistent policy application, and a lack of coordinated European-wide support mechanisms.

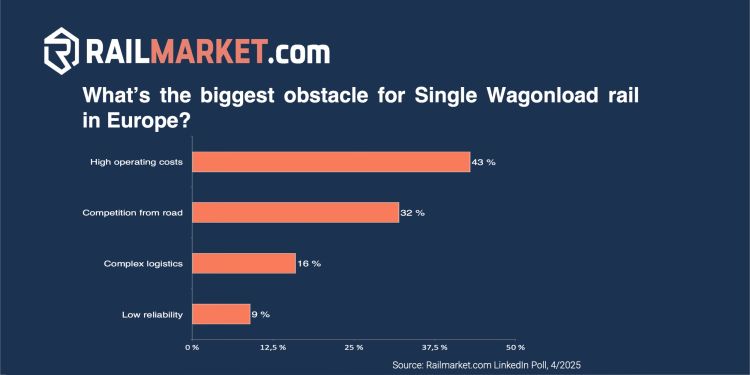

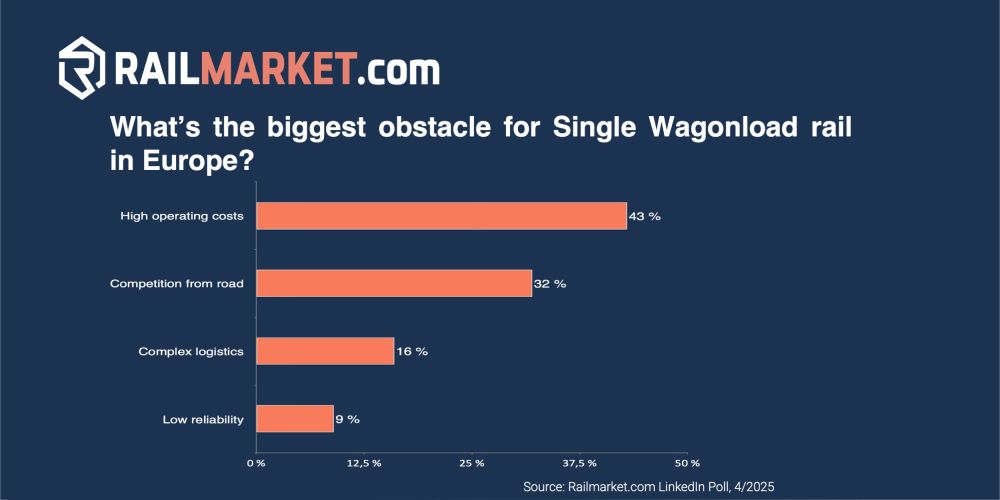

The quick poll social media results said that the biggest challenges in SWL have been high operating costs, complex logistics, competition from road and low reliability. Therefore Railmarket addressed the operators that still provide this service in Europe and here are their answers:

ZSSK CARGO (Slovakia):

ZSSK CARGO confirms that high operating costs and logistical complexity are tightly interconnected and reflective of the current SWL system. According to the company, these conditions make SWL particularly unappealing for private rail freight companies, leaving national carriers responsible for the service. The operator sees continued demand from sectors such as timber, scrap metal, construction materials, and chemicals, but stresses that profitability remains difficult without government support.

Additional challenges identified include the economic strain of modernizing diesel locomotives and freight wagons, which are critical to non-electrified operations and shunting duties. ZSSK CARGO argues that coordinated EU-level support is necessary, not only through infrastructure access discounts but also through policies mandating equal treatment between road and rail, and the internalization of external costs from road transport. In its view, existing measures in Slovakia are either temporary or insufficient.

To remain competitive, the company is focusing on regional consolidation strategies such as attraction zones and intermediary storage facilities for bundling shipments into block trains. ZSSK CARGO also highlights the potential for greater synergy between railway sidings and new industrial infrastructure, suggesting developers be required to integrate rail connections into new logistics hubs.

DB Cargo (Germany):

DB Cargo aligned its internal assessment with the community poll conducted by Railmarket News. The company indicated that digitalization is key for the future of SWL, particularly through the introduction of Digital Automatic Coupling (DAC). Although not quantifying specific obstacles, DB Cargo stated that network optimization has already been implemented to improve service reliability. Nonetheless, public financial support remains necessary to maintain service viability.

Rail Cargo Group (Austria):

According to Rail Cargo Group, road transport presents the most severe threat to SWL’s competitiveness. While operating costs are high, their impact is intensified by increasing pressure from road logistics. The group considers logistics complexity and declining reliability—caused in part by large railways withdrawing from the SWL sector—as central challenges.

Rail Cargo Group underscores the importance of high volumes for offsetting fixed infrastructure costs, and views single wagonload transport as a core offering, particularly for Austrian and Hungarian industry. However, it points out that without transnational coordination and targeted support mechanisms, the system cannot remain sustainable. Consolidation through multifunctional terminals and fixed-schedule feeder services (TransFERs) is cited as a way to improve efficiency and coverage.

Key commodities include paper, timber, scrap, building materials, and waste. The company also sees value in combining conventional freight wagons with intermodal logistics such as swap bodies.

SBB Cargo (Switzerland):

SBB Cargo referred to its published position paper on framework conditions for Swiss freight transport, where issues such as cost recovery, public service obligations, and investment planning are discussed. While not commenting specifically on the Railmarket News poll, the Swiss operator has previously emphasized the need for long-term political commitment and stable regulatory frameworks to support domestic and international freight solutions including SWL.

Rail Cargo Hungaria (Hungary):

Rail Cargo Hungaria agrees with the social media poll results and adds further considerations. The ongoing construction, renewal, and maintenance of railway lines across Europe severely limit throughput capacity, further diminishing the competitiveness of the SWL segment compared to road transport.

The Hungarian operator firmly believes in the future of SWL but emphasizes the necessity of sustained state aid. Achieving the EU’s goal of a 30% rail freight share by 2030—currently around 17%—requires significant changes, development in the transport network, and a decisive shift from road to rail.

To improve profitability, Rail Cargo Hungaria suggests regulation of road transport, alongside technical development, infrastructure renovation, and proper maintenance, including marshalling yards and loading areas. The operator enhances competitiveness by digitizing goods handling processes, developing an integrated train management system, and using energy-efficient locomotives.

Currently, Rail Cargo Hungaria's main commodities in SWL include wood, hazardous goods (fuels, gases), scrap iron, and electro-mobility components, with battery transport identified as particularly promising.

Participation and omissions

While ZSSK CARGO, DB Cargo, Rail Cargo Group, and SBB Cargo provided insights, several large operators - Green Cargo, ČD Cargo, SNCF, and Lineas - did not submit responses.

Contextual backdrop

The European Commission’s White Paper on Transport (Transport 2050) continues to push for a modal shift away from road to more sustainable forms of transport. SWL services are referenced in this framework as an integral part of the strategy. However, as multiple responses suggest, the future of SWL services depends not only on operational improvements but also on comprehensive policy implementation and financial mechanisms applied consistently across Europe.